Tags

How I learned about Spending Habits

How does one learn about spending habits? This is a question that has had a multi-layer answer for me over the years. First of all, I didn’t know what spending habits were, and didn’t know that mine were questionable. In the past post I used the term “creative financing.” What that meant for me, for most of my adult life, was to manipulate my financial affairs. I thought I was being clever, and most of the time (emphasis on ‘most’), I got away with it. See, if I was getting paid on Friday and Tuesday or Wednesday I’d run out of essentials, like milk, cereal, bread, lunch meat – things kids need to make breakfast or lunch, I would write a check at the grocery and hold out hope that the check I wrote would not clear the bank before I could deposit my paycheck. (You see, kids, once upon a time, there was no such thing as direct deposit – you had to wait until your boss handed out checks on Friday morning, and during lunch time, you had to drive to your bank, park the car, walk into the bank, get in line behind all the other folks who got paid, and actually deposit your check at a counter, with a bank employee. Seriously. I’m not making this up. Go ask your mom, or your grandpa.)

I had no idea how I kept running out of money. I didn’t keep track of my expenses. (Although I do vaguely remember my dad once sitting me down and explaining to me about budgets and expenses and stuff like that. I was 17, so it got filed away somewhere under ‘Dad’s Advice’ and I remembered it when I needed to share it with my kids.)

My first lesson in spending habits: Write down every single thing I spent money on – EVERYTHING. Buy a latte at Starbucks? Write it down. Donate two dollars to the lady outside of the grocery? Track it. Every utility, every bottle of water, every vending machine purchase – if you use a debit card, cash out of pocket, or write a check, you write that shit down. For 30 days. Trust me. This one exercise will open your eyes to where all the money goes.

My second lesson in spending habits: Once you realize where it’s all going, only spend as much as you make. Weird, right? Isn’t that what those credit cards are for? (No. The answer is NO. If you don’t have money left over after paying all your expenses each time you get paid, you have no business using a credit card YET.)

“Expenses? Income? What the heck is she talking about?” Okay, income is your pay. The money Coming In. Expenses is the money going out. (Some of you are thinking of leaving now, but trust me, LOTS of people do not know this, cannot grasp this concept. I mean, have you looked at the United States budget?)

I read Rich Dad, Poor Dad when I was 36 or so. Robert Kiyosaki suggested that a person save 10% of their income, give 10% to charity, and invest 10%, leaving 70% of that income for all their expenses. My first thought was, “Ten Percent? He’s kidding, right?” I gave no further thought to this idea at that time. Times have changed.

In 2009, I had to get things under control – my spouse lost his job and would be unemployed for 20 months. I read a book by Suze Orman titled 9 Steps To Financial Freedom. I will add that I read it in secret (so many secrets) to avoid being challenged should I choose to implement some of the suggestions. The first suggestion was Track Your Spending. Sure, tell the kids that chocolate chip cookies are not a necessity.

Remember when I wrote that I had to pay off $11,000 in credit card debt from 2003 to 2006? I truly believed that all that debt came from one poor business decision. Nope, I spent money like people breathe air. I used credit cards and justified their existence with things like, “Do you know how much kids cost to raise?” and “We needed a new car.” I found out later that I made enough money, but I did not live within my means.

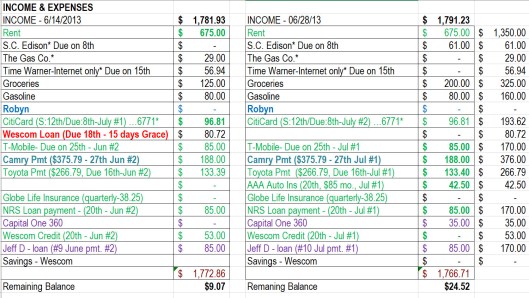

Here’s a shot of a budget that I used consistently from 2008 until 2015 (sorry, Spending Plan. A friend who attended Debtors Anonymous taught me that phrase. Apparently, the members of that 12 step group felt that the word ‘budget’ was deceiving, and spending was calling it like it was.):

I made enough to live well and pay all those freaking payments. I learned how to spend responsibly. This took some time to learn. With this spreadsheet (that I created all mby myself) I knew how much was coming in and when, and I knew when every bill was due and how much was due. (Plus, I am an Excel geek) Remember that self-discipline I mentioned? Having control of my finances was THAT important to me. I was tired of having no extra money, having really low credit scores, and always being in debt.

My brother taught me the ‘credit card’ shuffle to pay off the credit cards faster by opening new credit card account and transferring balances from cards with high interest to the new cards that offered incentives like Zero Interest for 18 months just for opening an account. (Only do this if you have learned to practice that self-discipline. Otherwise, you are just transferring a bad habit to a new card.)

I had it under control for a long time – BUT, because I still didn’t understand the connection between the past and my present, and emotions and deprivation, I still had a hard lesson to learn (several, in fact) about WHY I continued to have issues with money.

I too have had issues with my own spending habits. My purchases can sometimes be irrational. I’ve opened up credit card accounts. I currently have two credit cards that I owe money on. I do not own a vehicle because I can’t afford it. I used to buy a lot of things from Amazon. They were mostly knowledge-based purchases. Items that I needed. I’ve even had to use a check to get my medicine from the pharmacy. Nobody takes checks anymore so I was terrified that it wouldn’t work. I am mostly in debt due to my student loans. I also have old medical bills that definitely need my attention and are starting to affect my credit. Currently, I am not working. My husband is doing his best to bring in some money and take care of our expenses.

LikeLike